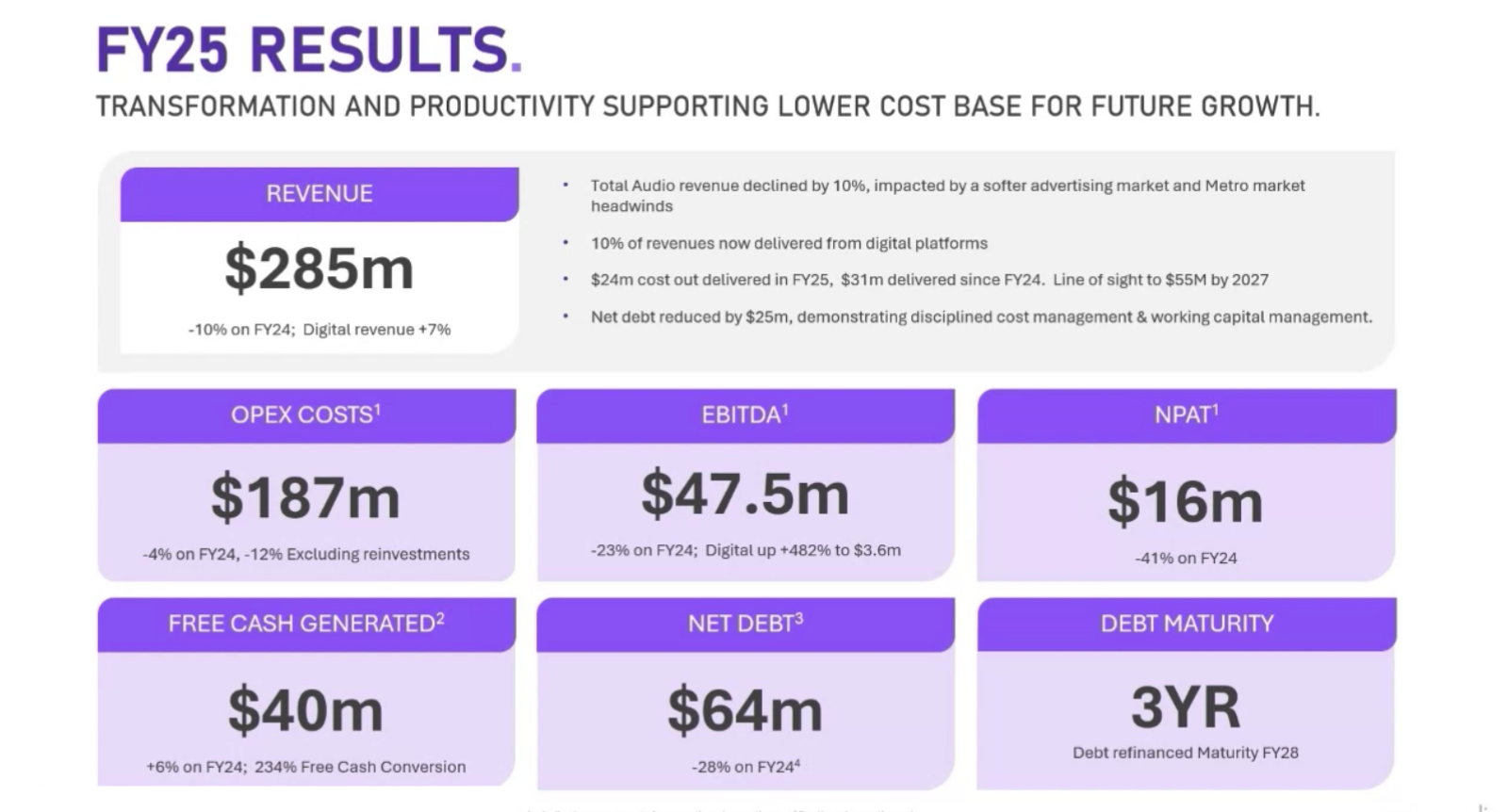

ARN Media has reported a 23% fall in underlying EBITDA for FY25, as the audio group enters what CEO Michael Stephenson describes as the execution phase of a broader strategic reset.

Underlying EBITDA dropped from $61.8 million to $47.5 million, while total revenue declined 10% to $285.2 million. Statutory EBITDA fell 27% to $45.7 million.

The result reflects a year of revenue pressure in metro radio, offset by cost-cutting, debt reduction and a renewed push into digital.

At the time of publication, the company’s share price was $0.37.

Source: ARN

Metro softness drives the earnings slide

The most immediate pressure came from metro advertising.

During this morning’s earnings call, Chief Financial Officer Alexis Poole said: “While we are disappointed with a 16% decline in metro, which reflects softer advertising conditions and changing advertiser preferences, we are also taking decisive action.”

That decline fed directly into the earnings compression. Revenue fell 10%, but EBITDA declined more than twice as fast, underscoring the radio model’s fixed-cost nature.

Operating costs were reduced 4% to $187 million, with $24 million in savings delivered during FY25. ARN has now identified $55 million in cost reductions across FY24–FY27, with $31 million already realised.

More tightening is still to come.

Source: ARN

Digital growing, but still a minority of revenue

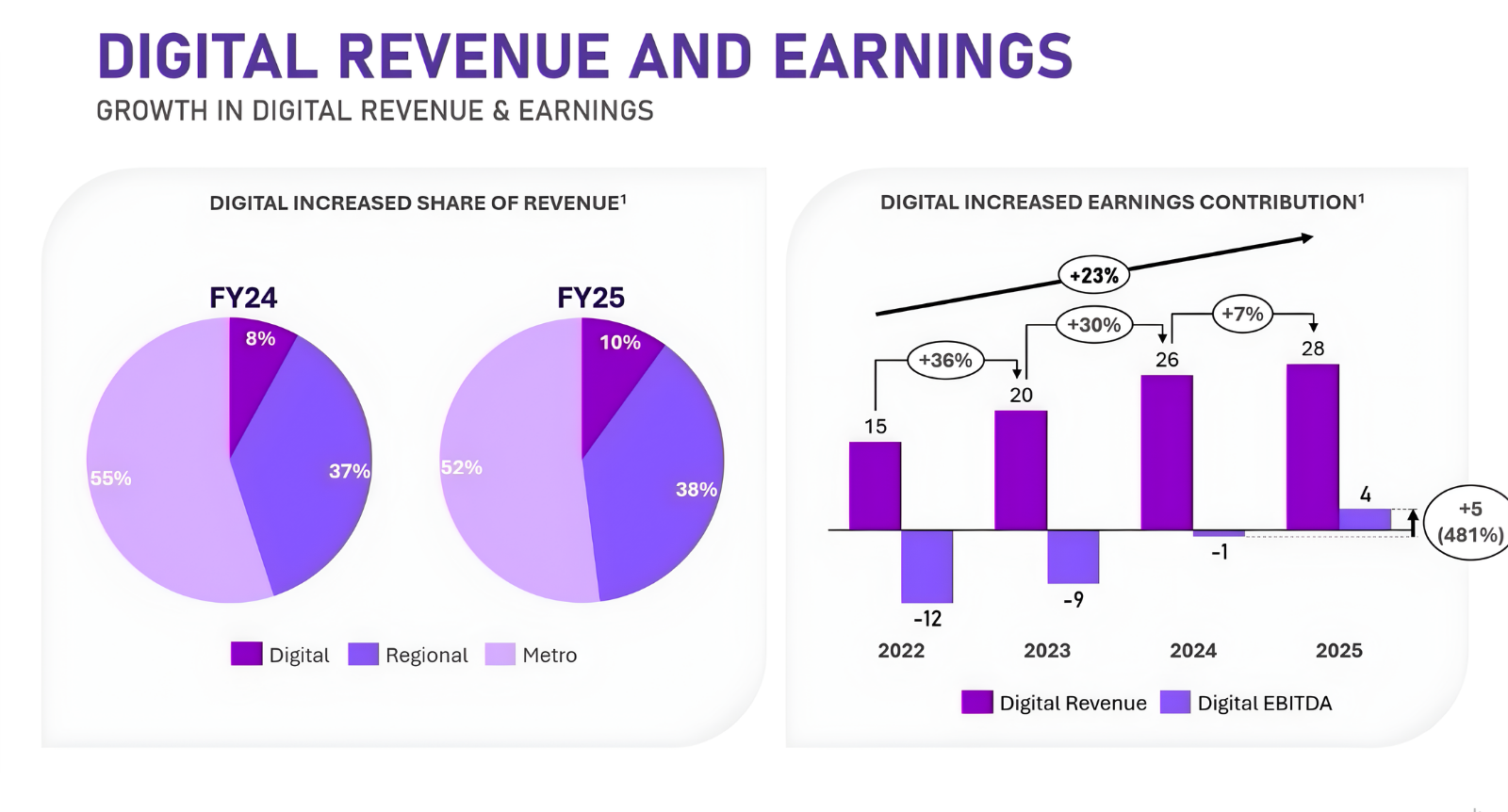

Digital revenue grew 7% to $27 million in FY25, now representing 10% of group revenue.

Poole said digital “is becoming materially more profitable.”

“In FY25, digital audio revenue reached $27 million, growing 7%, driven by the doubling of live streaming revenue,” she said.

However, podcast revenue declined after ARN exited lower-margin third-party agreements.

“Digital 7% growth was achieved despite podcast revenue decline, following deliberate exit of low margin third party agreements with onerous minimum revenue guarantees,” Poole said.

“A conscious trade-off was made to improve earnings, prioritise content ownership, reinvestment into ARN-owned podcasts and a deeper integration into the iHeart ecosystem. This is an example of our improved financial discipline.”

Even with growth, digital remains a small portion of overall revenue – a structural reality that continues to expose ARN to metro radio volatility.

Michael Stephenson and Alexis Poole during the ARN earnings call. Source: ARN

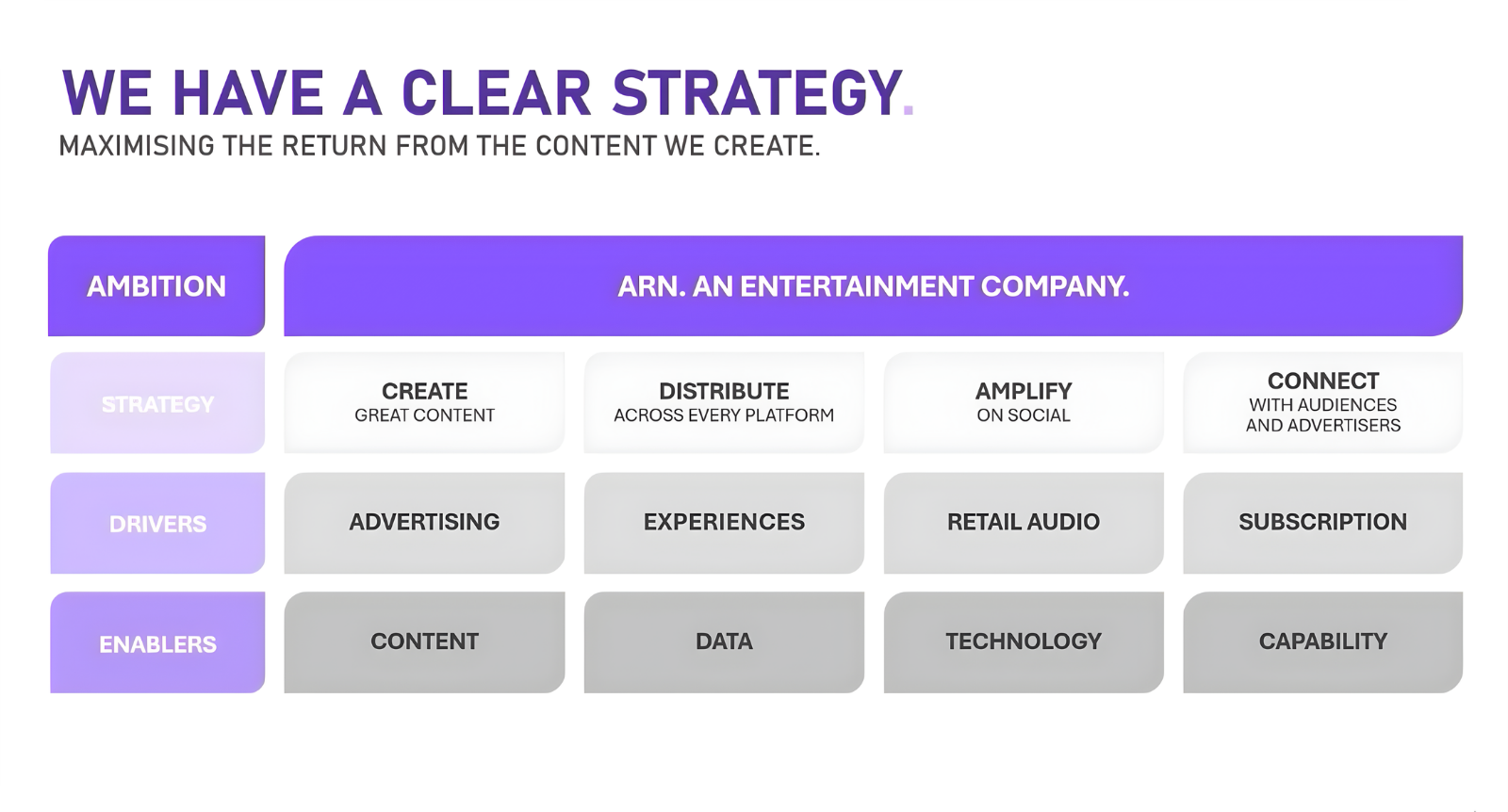

The strategy: build beyond radio

Stephenson has framed the reset as deliberate and disciplined.

“We have a very clear strategy. Create great content, distribute it broadly, amplify it on social platforms to engage our audiences, and, importantly, our advertisers. That’s our plan,” he said.

“Our focus is on maximising the return on our existing content and talent investment by using our leading radio brands, our number one radio shows, and our radio stars to create content for every other platform. Content for radio, content for podcasts, content for video, and content for social platforms.”

Radio, he said, remains foundational.

“But what we’re building around it is something bigger. A platform that brings together audio, video, social and live experiences to create one connected entertainment ecosystem.”

Stephenson pointed to audio-video convergence as a medium-term opportunity, extending radio and podcast assets into video formats using existing studio and technology capability, “importantly with no incremental cost.”

“This strategy is expected to diversify revenue whilst improving the long-term monetisation of core audio assets,” he said.

Michael Stephenson during the ARN earnings call. Source: ARN

The $200 million talent bet in sharper focus

The earnings slide also sharpens scrutiny on ARN’s record-breaking $200 million, 10-year deal with Kyle Sandilands and Jackie ‘O’ Henderson.

The Sydney breakfast show remains a ratings force in its home market, but expansion has been incremental rather than national. Melbourne performance remains modest, while Perth will receive the show via DAB+.

In a year where EBITDA fell 23%, major talent investments inevitably attract closer investor attention.

Stephenson has made clear the shift now is from redesign to delivery.

“We’ve obviously gone through a complete organisational redesign. We’ve put a new team in place. We’ve got a very clear strategy which I’ve outlined today to you in this presentation, communicating that to our teams broadly, and that will begin to execute,” he said.

“We’re in the executional phase and the vast majority of my time is spent on how we execute that plan across our entire business, diversify revenues and generate greater profits for our shareholders.”

Cash flow up, debt down – dividends paused

Despite earnings pressure, free cash flow rose 6% to $40 million, with free cash conversion reaching 234%.

Net debt was reduced 28% to $63.8 million, and debt facilities were refinanced and extended by three years.

However, the Board has suspended dividends while non-core assets are divested.

The message is clear: balance sheet repair and reinvestment take precedence over yield.

Outlook: flat market, execution critical

ARN expects the total audio advertising market to be flat in FY26, with low single-digit declines in radio offset by mid-to-high teens growth in digital.

Stephenson has acknowledged that the revenue mix must change.

“Today, whilst 40% of our audience is delivered on a digital platform, only 10% of our revenue is digital,” he said.

“Over time, any decline that we might see in traditional revenues will be more than offset by the growth in digital revenue.”

That ambition now defines the task ahead.