In 2020, the overall entertainment and media industry in Australia declined -3.6 percent – an unprecedented drop that had an asymmetrical impact across the sector, reports the new edition of PwC Australia’s annual Outlook report into the entertainment and media sector.

Key findings

• PwC reports despite the challenges of 2020, 2021 is showing signs of a strong recovery for most, although the shadow of COVID-19 has not yet left the sector

• Consumer revenue is set to grow to A$52.6 billion in 2025, at a CAGR of 3.3% while advertising revenue is set to grow to A$19.6 billion in 2025, at a CAGR of 2.6%

• Internet advertising recorded growth of 3.3% in 2020 reaching A$9.3 billion and is expected to grow at 5.5% over the forecast period to 2025 based on the midpoint scenario

• Streaming Video On Demand (SVOD) revenues will grow at a 20.4% CAGR through to 2025, becoming a US$81.3 billion industry globally, and an estimated A$3.3 billion in Australia

• Broadcast Video on Demand (BVOD) revenue grew 38.8% in 2020, and will continue to grow with a CAGR of 32.7% over the forecast period to 2025, continuing to grow its overall share of attention

• Out-of-Home (OOH) saw a 39.0% decrease in year-on-year revenue to A$772 million, although it is starting to see a recovery, with year-on-year revenue continuing to improve since the second quarter of 2020 (April – June)

Advertisers looked for ways to stay top of mind with consumers as people retreated to their screens and devices while spending more time at home in 2020. The 20th edition of PwC Australia’s annual Australian Entertainment and Media Outlook revealed that to the end of December 2020, total Australian advertising spend contracted by 8.0 percent to A$15.4 billion, and consumer spend dropped by 1.9 percent to A$42.5 billion.

The hardest-hit sectors were filmed entertainment with a 41.0 percent fall from A$2.2 billion to A$1.3 billion, and Out-of-Home (OOH) falling -39.0 percent from A$1.3 billion to A$772 million. Where some sectors saw an increase in readership, such as digital news, or an increase in audience, such as free-to-air television (FTA), revenue was lean for much of the calendar year, until a late surge in November and December as the country emerged out of lockdown.

One of the few winners off the back of the pandemic was internet advertising, which saw an increase of 3.3 percent from A$9.0 billion to A$9.3 billion in 2020. In the consumer category, streaming services did well throughout the calendar year, with Streaming Video on Demand (SVOD) increasing both subscribers and users, while Broadcast Video On demand (BVOD) services increased both audience and advertising revenues, albeit off a lower base.

Justin Papps, PwC Australia partner and Australian Entertainment and Media Outlook editor, said “The pandemic triggered the sharpest contraction in Australian entertainment and media revenues in the history of the report. While the contraction impacted the whole market, it was clear that some sectors were hit harder than others. However, even with the COVID cloud still lingering, momentum was strong for the sector going into the first quarter of the 2021 calendar year.

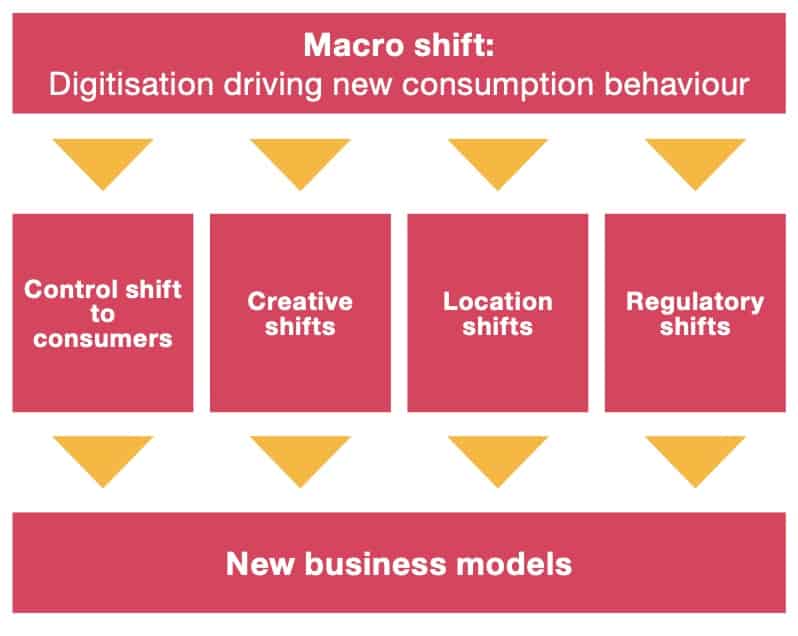

“We see five major power shifts that are impacting the entertainment and media landscape to varying degrees. The overarching shift is undoubtedly sustained digital disruption. This shift is then enabling significant power shifts into the hands of consumers, a shift of creative power to content originators, a shift based on location and the need for anywhere, anytime access and finally, regulatory shifts that put privacy and data monetisation under the microscope. Even with these shifts, the stability or resilience of the market overall should not be underestimated. The contraction of 2020 is giving way to a solid rebound this year, and a return to 2019 revenue levels within the next few years for most parts of the industry, if not sooner.”

PwC: Ongoing migration to digital consumption across all segments

As consumers stayed home and in-person venues shut down, use of digital services soared. While cinema box office revenues fell -67.4 percent in 2020, this was contrasted by increased availability, sector breadth and catalogue depth of the SVOD players, increased BVOD usage, and the sustained growth of the gaming and esports sector.

Australia saw significant growth as established players such as Netflix, Amazon and Stan expanded their content libraries. Binge and BritBox also entered the market, and relative newcomers such as Disney+ used the opportunity to try different business models, including Premium Video on Demand (PVOD) for new release movies.

Consumers controlling media presents challenges for advertisers

With consumers more firmly in control of how they spend their time and money, especially during the pandemic, traditional platforms that advertisers buy to reach audiences at scale, including television, newspapers and OOH all had significant competition for their share of consumers’ attention. The range of competing media platforms and channels also added to the complexity of delivering a consistent message over time.

Media consumption locations are changing dramatically

Total internet access revenue showed marginal growth in Australia in 2020 while demand for at-home connectivity rose, driven by a 38 percent growth in download volumes. The total Australian internet access market was worth A$30.1 billion in 2020, a year-on-year growth of 1.14 percent.